Introduction

You've decided to lease your land for hunting. You've done your research on liability laws, you're drafting a solid lease agreement, and you're ready to start earning income from your property. But then someone asks: "Does your insurance cover this?"

You pause. Your farm insurance policy is thick. You've never actually read through every clause. You assume you're covered... but are you really?

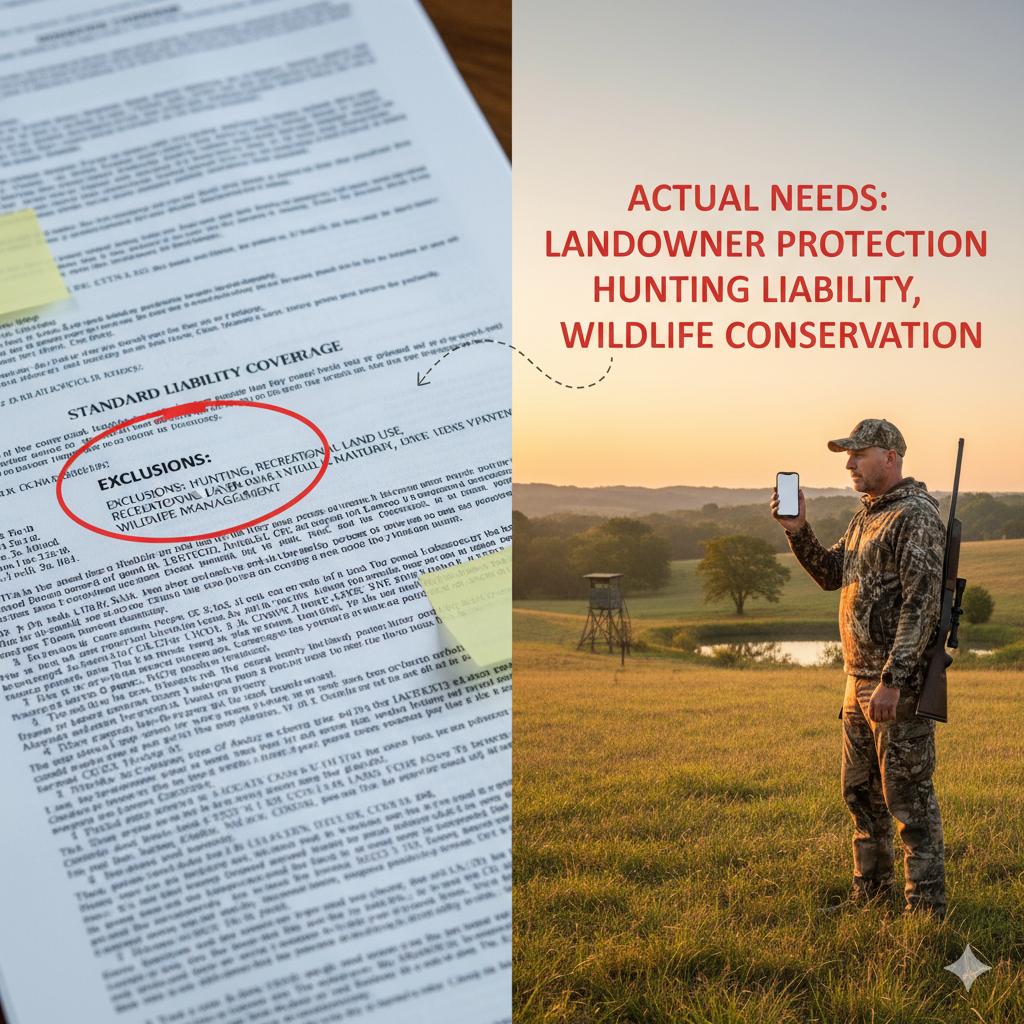

Here's the uncomfortable truth most landowners discover too late: Your farm or homeowner's insurance policy probably does NOT cover hunting leases. Especially if you're charging money for access.

The good news? Once you understand what's covered (and what isn't), getting the right protection is straightforward and affordable. This guide will walk you through everything you need to know about hunting lease insurance so you can lease your land with confidence.

Does Your Current Insurance Cover Hunting Leases?

Let's start by examining what your existing insurance policies likely do—and don't—cover.

Homeowner's Insurance: Probably Not

Standard homeowner's insurance policies typically cover:

- Personal liability for accidents on your property to invited guests

- Premises liability for non-commercial activities

- Medical payments for injured visitors

What homeowner's policies usually DON'T cover:

- ❌ Commercial activities (including paid hunting leases)

- ❌ Injuries related to inherently dangerous recreational activities

- ❌ Liability for large undeveloped acreage

- ❌ Business income or commercial operations

The bottom line: If you're charging for hunting access, your homeowner's policy likely considers this a commercial activity and won't provide coverage.

Farm and Ranch Insurance: Maybe, But Probably Not

Farm and ranch insurance policies are more nuanced. Some agricultural policies include:

- Farm liability coverage for normal farming operations

- Coverage for agritourism activities (depending on the policy)

- Premises liability for your agricultural property

However, most farm policies specifically EXCLUDE:

- ❌ Hunting leases and recreational land use for profit

- ❌ Liability for injuries during sporting activities

- ❌ Commercial recreation enterprises

Some farm insurance policies offer optional "agritourism" or "recreational use" endorsements, but these must be specifically added to your policy—and they may still exclude hunting-related activities.

Critical question to ask your agent: "Does my farm liability policy cover injuries or accidents that occur during paid hunting activities on my property?"

Umbrella Policies: Additional Protection, But Check Exclusions

Umbrella liability policies provide extra coverage beyond your primary insurance limits. If you have a $1 million farm liability policy and a $2 million umbrella policy, you'd have up to $3 million in total coverage.

Do umbrella policies cover hunting leases?

It depends entirely on:

- Whether your underlying policy (farm or homeowner's) covers the activity

- The specific exclusions in your umbrella policy

- Whether the umbrella considers hunting leases a commercial activity

Generally, if your primary policy doesn't cover hunting leases, your umbrella policy won't either—because umbrella coverage only kicks in after your primary coverage is exhausted.

What is Hunting Lease Liability Insurance?

Hunting lease liability insurance is specialized coverage designed specifically to protect landowners who lease their property for hunting. It's sometimes called:

- Recreational use liability insurance

- Landowner hunting liability coverage

- Agritourism hunting insurance

What Does It Cover?

A typical hunting lease liability insurance policy provides:

✅ Bodily injury liability: Covers medical expenses, legal defense, and settlements if a hunter is injured on your property

✅ Property damage liability: Covers damage caused by hunting activities (though the hunter's own equipment is not covered)

✅ Legal defense costs: Covers attorney fees and court costs if you're sued, even if the lawsuit is frivolous

✅ Settlement and judgment payments: Pays out settlements or court-ordered judgments up to your policy limits

✅ Medical payments: Covers immediate medical expenses for minor injuries without requiring a lawsuit

Policy limits typically range from:

- $500,000 to $2,000,000 per occurrence

- $1,000,000 to $3,000,000 aggregate (total for all claims in a policy period)

What Doesn't It Cover?

Like all insurance, hunting lease liability policies have exclusions:

❌ Intentional acts: Deliberate harm you cause to someone

❌ Gross negligence: Extreme recklessness or willful disregard for safety

❌ Your own injuries: The policy covers hunters and guests, not you as the landowner

❌ Property damage to your own land: Your land, structures, or equipment

❌ Business interruption: Lost income if you can't lease the property

❌ Professional services: If you're providing guided hunts or professional services, you'd need additional coverage

How Much Does Hunting Lease Liability Insurance Cost?

One of the best parts about specialized hunting lease insurance? It's remarkably affordable.

Typical Premium Costs

For most landowners, hunting lease liability insurance costs:

- $300 to $600 per year for $1,000,000 in coverage

- $500 to $900 per year for $2,000,000 in coverage

Factors that affect your premium:

- Total acreage being leased

- Number of hunters allowed on the property

- Types of game being hunted (deer, waterfowl, big game, etc.)

- Whether you provide any structures (blinds, tree stands, lodging)

- Your location and state regulations

- Your claims history

Cost-Benefit Analysis

Let's put this in perspective:

If you lease 100 acres at $10/acre/year, you're earning $1,000 annually. A $400 insurance policy is 40% of that income, but it provides up to $1,000,000 in protection.

If you lease 200 acres at $15/acre/year, you're earning $3,000 annually. That same $400 policy is only 13% of your income.

For most landowners with moderately priced leases, insurance costs represent 10-25% of gross lease income—a reasonable expense for complete peace of mind.

Where to Get Hunting Lease Liability Insurance

Several insurance providers specialize in recreational use and hunting lease liability coverage:

National Providers:

- Great American Insurance Company - Offers specialized recreational use liability

- RLI Insurance Company - Known for agritourism and recreational property coverage

- Markel Insurance - Provides hunting and recreational land use policies

Through Insurance Agents:

- Independent insurance agents who specialize in farm, ranch, and agricultural insurance

- Agents who work with outdoor recreation and agritourism businesses

Industry-Specific Programs:

- Some state farm bureaus offer hunting lease insurance programs

- Hunting lease management companies sometimes offer group insurance programs

Should the Landowner or Hunter Get Insurance?

This is one of the most common questions landowners ask. The answer? Both.

Let's break down why each party should carry their own coverage and how these policies work together.

Why Landowners Should Carry Insurance

Even with a solid lease agreement and liability waivers, having your own insurance provides:

1. Defense Against Frivolous Lawsuits

Anyone can sue anyone for anything. Even if you have a rock-solid lease agreement, you still need to defend yourself in court. Your insurance covers legal defense costs, which can easily reach $50,000-$100,000 even if you win.

2. Protection If Your Lease Agreement Is Challenged

Courts sometimes invalidate liability waivers, especially if:

- The waiver language wasn't clear

- The hunter didn't understand what they were signing

- State law limits enforceability of waivers

Your insurance provides a backup layer of protection if your lease agreement doesn't hold up.

3. Coverage for Non-Hunter Incidents

What if a hunter's guest is injured? What if someone else (a hiker, neighbor, or trespasser) is hurt during hunting season and claims it was related to your hunting lease activities? Your insurance covers these scenarios.

4. Peace of Mind

The cost of insurance is minimal compared to the mental peace it provides. You can focus on managing your property and relationships with hunters instead of worrying about worst-case scenarios.

Why Hunters Should Carry Insurance

Hunters absolutely should carry their own liability insurance, and you should require it in your lease agreement. Here's why:

1. They're Responsible for Their Actions

If a hunter injures someone else, damages property, or causes an incident through their negligence, they're primarily liable—not you. Their insurance covers:

- Injuries they cause to other hunters

- Property damage they cause

- Accidental discharge incidents

- Tree stand accidents they're responsible for

2. It Protects You as the Landowner

When you require hunters to carry insurance and name you as "additional insured," you get an extra layer of protection. If someone sues both you and the hunter, the hunter's insurance responds first before your policy.

3. Most Hunters Already Have It

Many hunters don't realize they already have liability coverage through:

- Homeowner's or renter's insurance: Often includes personal liability coverage that extends to hunting activities

- Hunter's insurance: Specialized policies that cover hunting-related liability

- Sportsman's insurance: Coverage specifically designed for outdoor recreation

4. It Shows They're Serious and Responsible

Requiring proof of insurance helps you filter for professional, committed hunters who take safety seriously. It's a sign of a quality hunting partner.

How Both Policies Work Together

When both parties have insurance, here's typically how it works if there's an incident:

Step 1: The hunter's insurance is the "primary" policy. It responds first and covers their direct liability.

Step 2: If the claim exceeds the hunter's coverage limits, or if you're also named in the lawsuit, your landowner insurance kicks in as "secondary" coverage.

Step 3: Both insurance companies work together to defend the claim and minimize costs.

This layered approach means you have multiple lines of defense and significantly higher total coverage amounts.

What to Require from Hunters: Insurance Best Practices

If you're going to require hunters to carry insurance (and you should), here's exactly what to ask for:

1. Minimum Coverage Amounts

Specify in your lease agreement:

- Minimum liability coverage: $300,000 to $500,000 per occurrence

- Higher amounts for commercial/group leases: $1,000,000 per occurrence

These amounts should be clearly stated in your lease terms.

2. Certificate of Insurance

Before allowing any hunter on your property, collect a "Certificate of Insurance" (COI) from their insurance provider. This document proves they have active coverage and shows:

- Policy number and effective dates

- Coverage amounts

- Types of coverage included

- Insurance company contact information

3. Additional Insured Status

Ask to be named as an "additional insured" on the hunter's liability policy. This means:

- You're specifically listed as a covered party on their policy

- Their insurance will defend you if you're both sued

- You can receive direct notice if their policy is cancelled

Adding an additional insured typically costs the hunter nothing or a very small fee ($25-50).

4. Proof of Coverage Before Each Season

Don't just collect insurance once and forget about it. Require:

- Annual proof of insurance renewal

- Updated certificates if hunters change insurance companies

- Immediate notification if coverage is cancelled

Sample Lease Language

Here's example language you can include in your lease agreement:

"Lessee agrees to maintain comprehensive general liability insurance with minimum limits of $500,000 per occurrence and $1,000,000 aggregate throughout the term of this lease. Lessee shall provide Lessor with a Certificate of Insurance naming Lessor as Additional Insured before any hunting activities begin. Failure to maintain required insurance shall be grounds for immediate termination of this lease."

Special Considerations and Insurance Scenarios

Exclusive vs. Per-Person Leases

Exclusive leases (one person/group has sole access):

- Clearer insurance requirements—one party covers everyone in their group

- Lease holder is responsible for ensuring all their guests are covered

- Your insurance needs may be lower since you're dealing with one responsible party

Per-person leases (multiple individual hunters):

- Each hunter should carry their own insurance

- More certificates to collect and manage

- Higher potential complexity if multiple hunters are on property simultaneously

Seasonal vs. Year-Round Leases

Year-round leases:

- Ensure insurance coverage extends throughout the full year

- Consider off-season activities (scouting, trail maintenance, food plot planting)

- Your own policy should provide year-round coverage

Seasonal leases:

- Insurance can sometimes be tailored to the hunting season only

- Clearly define when the season starts and ends in your lease

- Verify coverage includes pre-season scouting and post-season activities

Leasing to Youth Hunters

When leasing to hunters under 18:

- Parents/guardians must sign the lease and carry the insurance

- Verify their homeowner's policy covers their minor children's hunting activities

- Consider requiring adult supervision be present at all times

- Some insurers have specific requirements for youth activities

Providing Lodging or Amenities

If you provide more than just land access:

- Lodging: May require commercial general liability or agritourism insurance

- Hunting blinds/stands you built: May increase your liability exposure

- ATV/vehicle rentals: Requires specialized equipment coverage

- Guided services: Requires professional liability insurance

Each of these additions increases complexity and may require separate or enhanced insurance coverage.

Do Recreational Use Statutes Eliminate the Need for Insurance?

A quick but important point: Even though your state's Recreational Use Statute provides liability protection, it doesn't eliminate the need for insurance.

Here's why:

RUS protections can be challenged:

- Courts may interpret statutes differently

- Exceptions exist for charging fees in many states

- Gross negligence can override RUS protections

Insurance covers more than just successful lawsuits:

- Legal defense costs even if you win

- Settlement negotiations to avoid court

- Peace of mind and professional claims handling

RUS and insurance work together:

- RUS provides the legal framework that limits liability

- Insurance provides financial protection and legal defense

- Together, they create comprehensive protection

Think of RUS as your legal shield and insurance as your financial armor. You want both.

Understanding Your State's Recreational Use Statute

Action Steps: Getting Properly Insured

Ready to ensure you have the right coverage? Follow these steps:

Step 1: Audit Your Current Insurance (This Week)

- Call your insurance agent and ask specifically about hunting lease coverage

- Review your farm/homeowner's policy declarations page

- Ask about agritourism or recreational use endorsements

- Document what is and isn't covered

Questions to ask:

- "Does my policy cover paid hunting leases?"

- "What happens if someone is injured during a hunting activity on my property?"

- "Do I have any commercial activity exclusions?"

- "What would it cost to add hunting lease coverage?"

Step 2: Get Quotes for Hunting Lease Insurance (This Week)

- Contact 2-3 insurance providers who specialize in hunting lease or recreational use coverage

- Get quotes for $1,000,000 and $2,000,000 coverage amounts

- Compare not just price, but coverage terms and exclusions

- Ask about bundle discounts if combining with existing policies

Step 3: Update Your Lease Agreement (Before Your Next Lease)

- Add clear insurance requirements to your lease template

- Specify minimum coverage amounts

- Include additional insured requirements

- Add language about proof of coverage and renewal requirements

Step 4: Create an Insurance Tracking System (Before Your Next Lease)

- Set up a folder (digital or physical) for insurance certificates

- Create a spreadsheet tracking: Hunter name, policy number, coverage amount, expiration date

- Set calendar reminders for policy renewal dates

- Establish a process for collecting certificates before granting property access

Step 5: Review Annually (Every Year)

Insurance needs change as your leasing operation grows:

- Reevaluate coverage amounts if you add more acreage or hunters

- Shop your policy every 2-3 years to ensure competitive rates

- Update requirements in your lease agreements as needed

- Review certificates and renew as policies expire

Conclusion: Insurance is an Investment, Not an Expense

When you're budgeting for your hunting lease operation, insurance might feel like just another cost cutting into your profits. But here's a better way to think about it:

Insurance is the price of peace of mind. It's what allows you to:

- Sleep soundly knowing you're protected

- Focus on building great relationships with hunters

- Grow your leasing operation with confidence

- Protect your family's financial future

For a few hundred dollars a year, you can eliminate the single biggest worry most landowners have about hunting leases. That's not an expense—that's a bargain.

The landowners who succeed in hunting leases are the ones who get the fundamentals right: solid lease agreements, proper insurance, and clear communication. Handle these basics, and everything else becomes easier.

Ready to start leasing your land the right way? HuntLease.co makes it simple to manage insurance requirements, connect with responsible hunters, and build a profitable hunting lease operation.

Get Started - Create Your Protected Listing Today

Frequently Asked Questions

Q: Can I just have hunters sign a waiver instead of requiring insurance?

A: Waivers are important, but they're not a substitute for insurance. Waivers can be challenged in court, and even if you're not liable, you still need to pay for legal defense. Insurance provides financial protection that waivers cannot.

Q: What if a hunter says their homeowner's insurance covers them—how do I verify this?

A: Always request an actual Certificate of Insurance from their insurance company. A verbal claim isn't sufficient. The certificate will show exactly what's covered and for how much.

Q: Is insurance more expensive if I allow rifle hunting vs. bow hunting only?

A: Generally no. Most hunting lease insurance policies cover all legal hunting methods. The policy is based on the activity (hunting) rather than the specific weapon used.

Q: What happens if a hunter's insurance expires mid-season?

A: Your lease agreement should state that maintaining continuous insurance is a requirement of the lease. If their insurance lapses, you have grounds to suspend their hunting privileges until they provide proof of renewed coverage.

Q: Do I need separate insurance for each property if I own multiple parcels?

A: Typically one policy can cover multiple properties you own. Discuss your specific situation with your insurance provider, as premiums may be based on total acreage or number of hunters across all properties.

Q: What if I only lease my land occasionally or to friends—do I still need insurance?

A: If money is changing hands, you should have insurance. "Occasional" leasing is still commercial activity. If you're truly providing free access as a gift, your risk is lower, but insurance is still wise protection.

Disclaimer: This article provides general information about hunting lease insurance and should not be considered professional insurance or legal advice. Insurance policies vary significantly by provider, state, and individual circumstances. Always consult with a licensed insurance professional to discuss your specific needs and ensure you have appropriate coverage.